Our purpose

Metals that matter,

for a healthier world

JM’s redefined purpose revolves around our global expertise in platinum group metals (PGMs) and the benefits these metals bring to people, communities and the environment. From providing air quality to enabling clean energy and transport to advancing cancer diagnostics, our PGM products and services are helping to create a healthier world.

Our purpose is about getting back to basics and simplifying our offer. Combined with our organisational restructure and strategic refresh, it provides a clearer sense of who we are, why we exist and what we need to do to deliver on our commitments. In short, it gives us the platform to perform; a foundation around which we can all align as we look to create a leaner, more focused and future-oriented JM.

Our behaviours

Safety first, always

Nothing comes before the safety of our people and operations

Work together

We combine our skills and expertise to solve problems and perform at our best

Take accountability

No excuses.

We take ownership and responsibility to deliver for our customers

Drive results

We strip out complexity and tackle issues head on, to unleash our full potential

£2,555m

In sales

c.9,500

Employees across 28 countries

(at 31st March 2026, inc. CT business)

£12,573m

Revenue

£340m

Underlying operating profit1

£168m

Free cash flow1

85%

Sales contributing to our four priority UN Sustainable Development Goals (SDGs)

New purpose.

Refreshed strategy.

Focused delivery.

Andrew Cosslett

Chair

Liam Condon

Chief Executive Officer

Alastair Judge

Chief Financial Officer

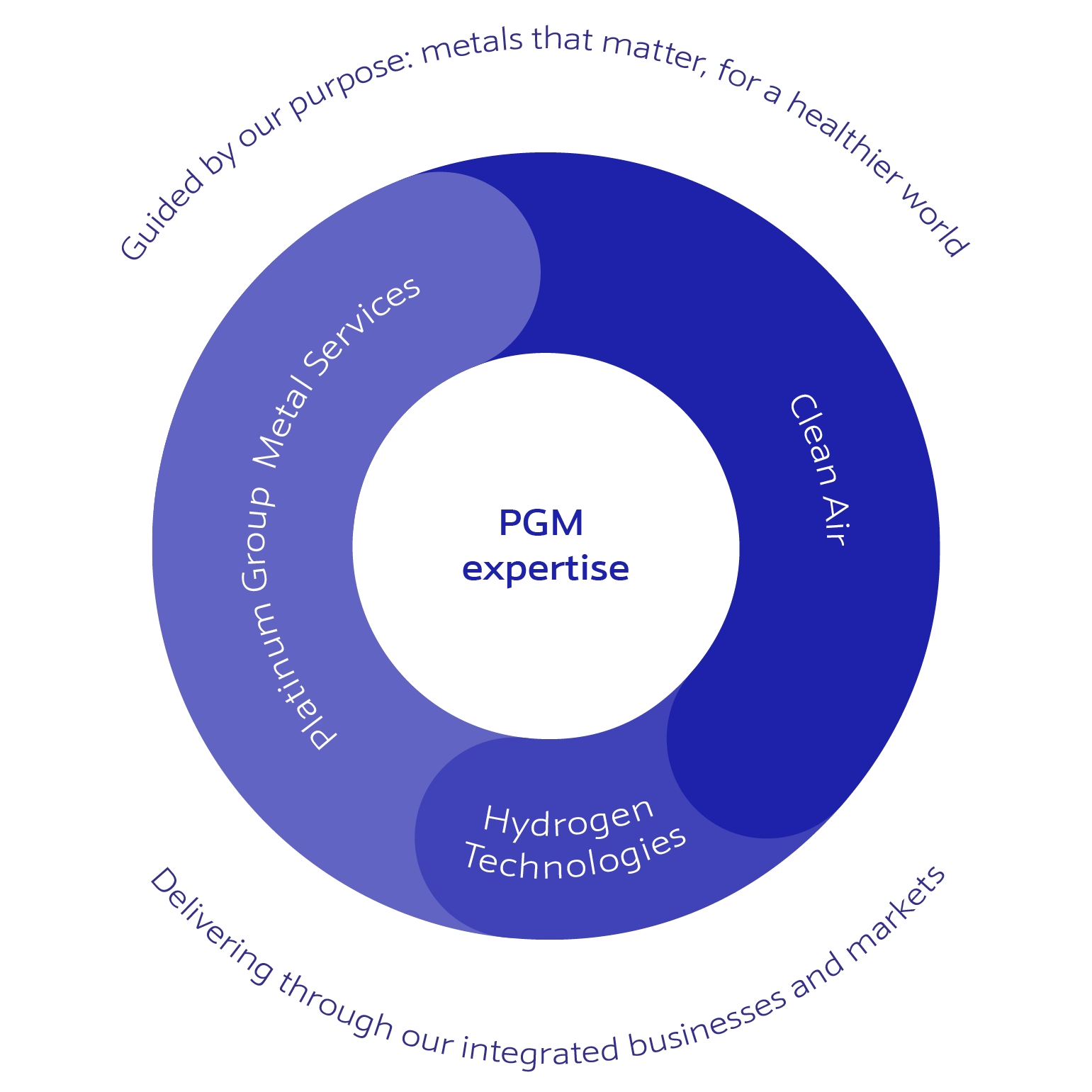

Leveraging synergies and competitive advantages

Expertise in metal chemistry

Everything we do across our three businesses is underpinned by our leadership in complex metal chemistry, catalysis and process engineering.

Mutual customers and partners

As our customers transition towards decarbonised energy systems, we provide a fully integrated and comprehensive offering through collaboration across our business units.

Shared technology and capabilities

We have approximately 2,400 R&D and engineering colleagues across all our businesses – with over 4,000 patents granted and more applications pending.

Foundational PGM ecosystem

We have deep insights into PGM markets through our Precious Metal Management team and our refining operations. A large share of the PGMs we use are sourced internally. This shared resource creates a resilient supply, lower exposure to price risk and efficient working capital.

Security of supply

Our customers count on us for a reliable supply of PGMs and recycling services. This is because we are the world's largest metal hub for PGMs, underpinned by our status as the leading recycler of PGMs.

A comprehensive sustainability offering

Every part of our business is committed to helping our customers adapt processes and products to reach the sustainability goals our society and planet are depending on.

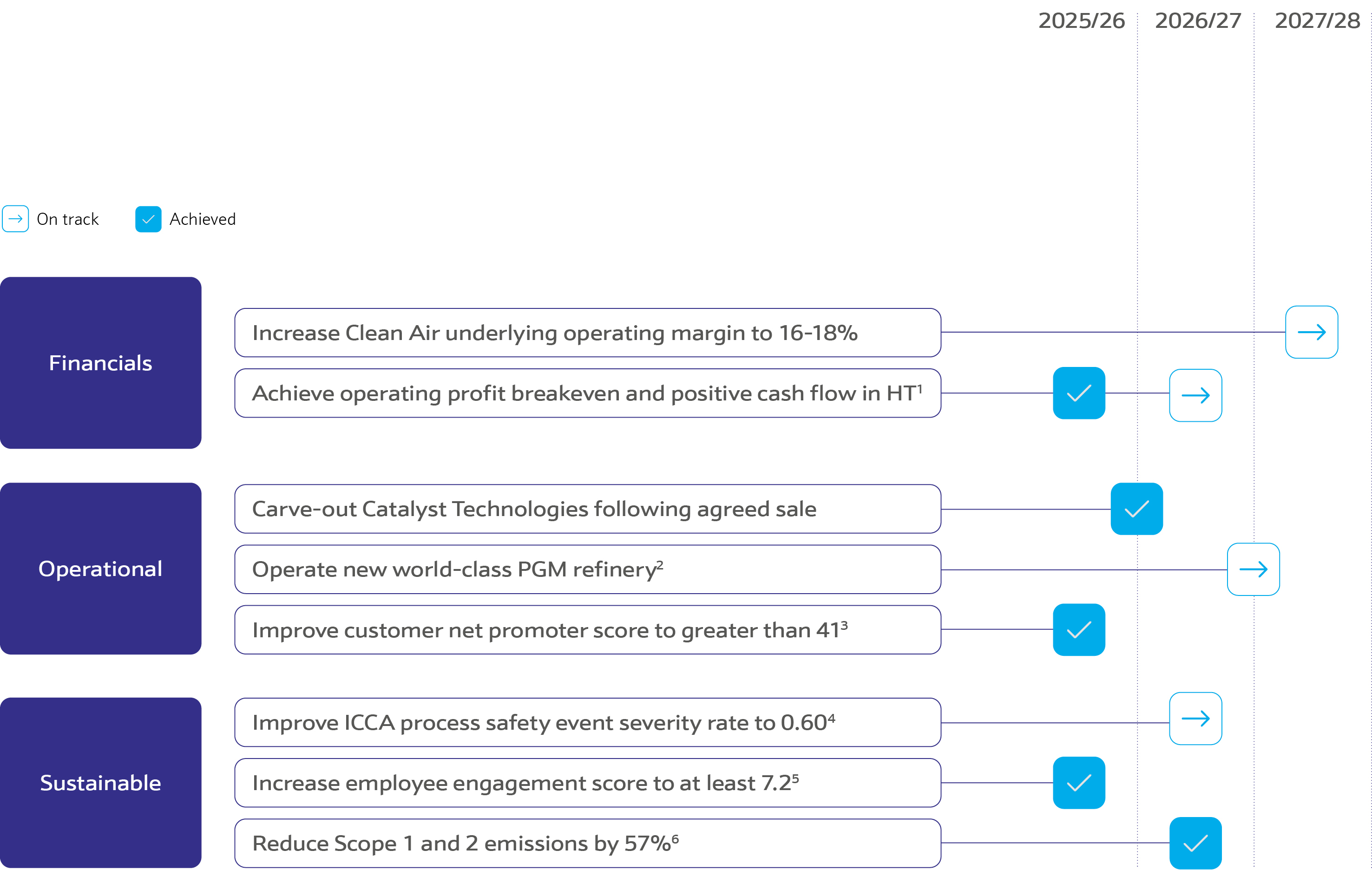

Revenue up, driven by higher precious metal prices.

Sales down 7% at constant currency excluding Value Businesses, driven primarily by Clean Air with lower volumes mainly reflecting market softness. Sales in PGM Services were also down and this more than offset growth in Hydrogen Technologies.

Operating profit decreased by 65%, due to a number of one-off items in the prior year. These include the profit on disposal of Medical Device Components, partially offset by higher major impairment and restructuring charges.

Good underlying performance with 6% growth, excluding the favourable impact of metal price (£24 million) and at constant foreign exchange rates (no impact). Strong cost savings and efficiencies across the Group enabling margin improvement.

Strong underlying cash flow generation driven by good underlying profit growth alongside reduced capital expenditure and continued reductions in working capital. (KPI linked to remuneration policy.)

Reported earnings per share decreased driven by major impairment and restructuring charges and deferred tax asset not recognised in the current year, resulting in a reported loss. (KPI linked to remuneration policy.)

Underlying earnings per share increased by 16% driven by a lower average number of shares following the share buyback in the prior year and solid underlying performance.

Dividend per share maintained at the same level as prior year.

The increase this year reflects changes in the overall sales mix. Differences in market performance led to a higher share of sales aligned with our four priority UN SDGs, with stronger contributions from areas more closely linked to these goals. Please see https://sdgs.un.org/goals for more details on the UN SDGs.

We saw a decrease in R&D spend against our priority UN SDGs as we continue to focus on UN SDG-aligned innovation.

Total Scope 1 and 2 GHG emissions decreased this year compared with the previous year, driven by reductions in Scope 1 emissions resulting from operational efficiencies and changes in product mix. (KPI linked to remuneration policy.)

Our GHG emissions from Scope 3 purchased goods and services were lower than last year, reflecting changes in purchasing behaviours and business requirements.

This financial year over 2.27 million tonnes of GHG emissions were avoided in customer products, aided by JM technologies or services. See our Sustainability Performance Databook for more details. (KPI linked to remuneration policy.)

The rate of recycled PGM content in our manufactured products was 73%, down from 76% in 2024/25, reflecting cyclical refining patterns and scheduled production downtime that increased the use of primary material.

The year-end total recordable injury and illness rate (TRIIR) is 0.47, above that of the past two years. The increase reflects higher slip, trip and fall injuries in January-February 2026, more ergonomic cases, and reduced office-based hours1 worked following organisational changes this year. (KPI linked to remuneration policy.)

Female representation at all management levels remains at 32% this year compared with the previous year. We remain committed to achieving our target of 40% by 2030. (KPI linked to remuneration policy.)

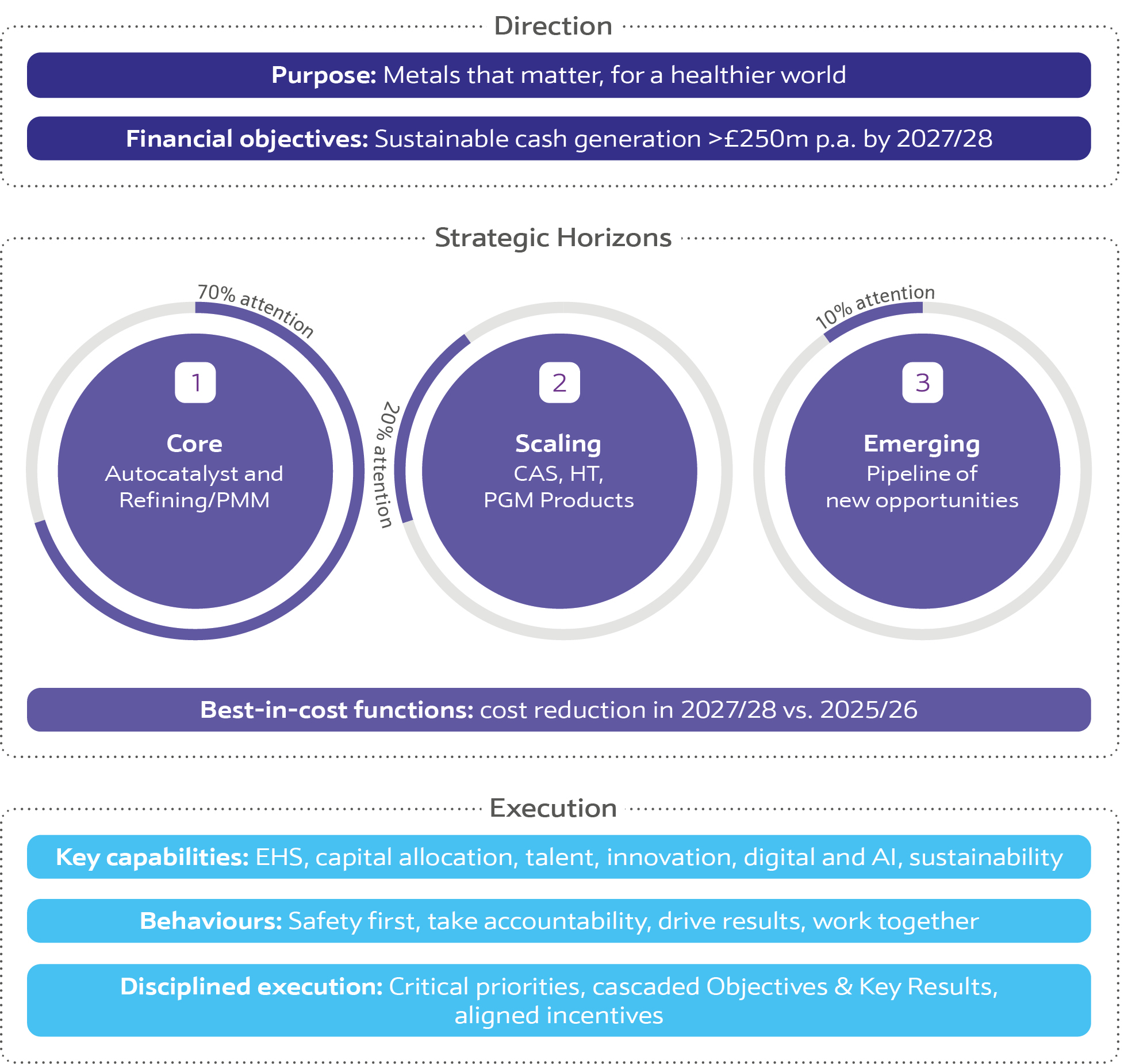

Strengthening our core.

Building for the future.

JM’s refreshed strategy aims to generate cash, drive growth and deliver sustainable value to 2035 and beyond.

In early 2026, we refreshed our strategy, looking to add greater depth, align with the market environment and present our short- to medium-term outlook for the business. Refocusing our activities, this strategic refresh supports the launch of the new JM: a highly focused, lean and cash-generative business delivering materially enhanced shareholder returns.

Our refreshed strategy is focused on ensuring longevity across our three strategic horizons, Core, Scaling and Emerging, with a commitment to generate a minimum of £250 million p.a. in cash and £200 million of shareholder returns in and beyond 2027/28.

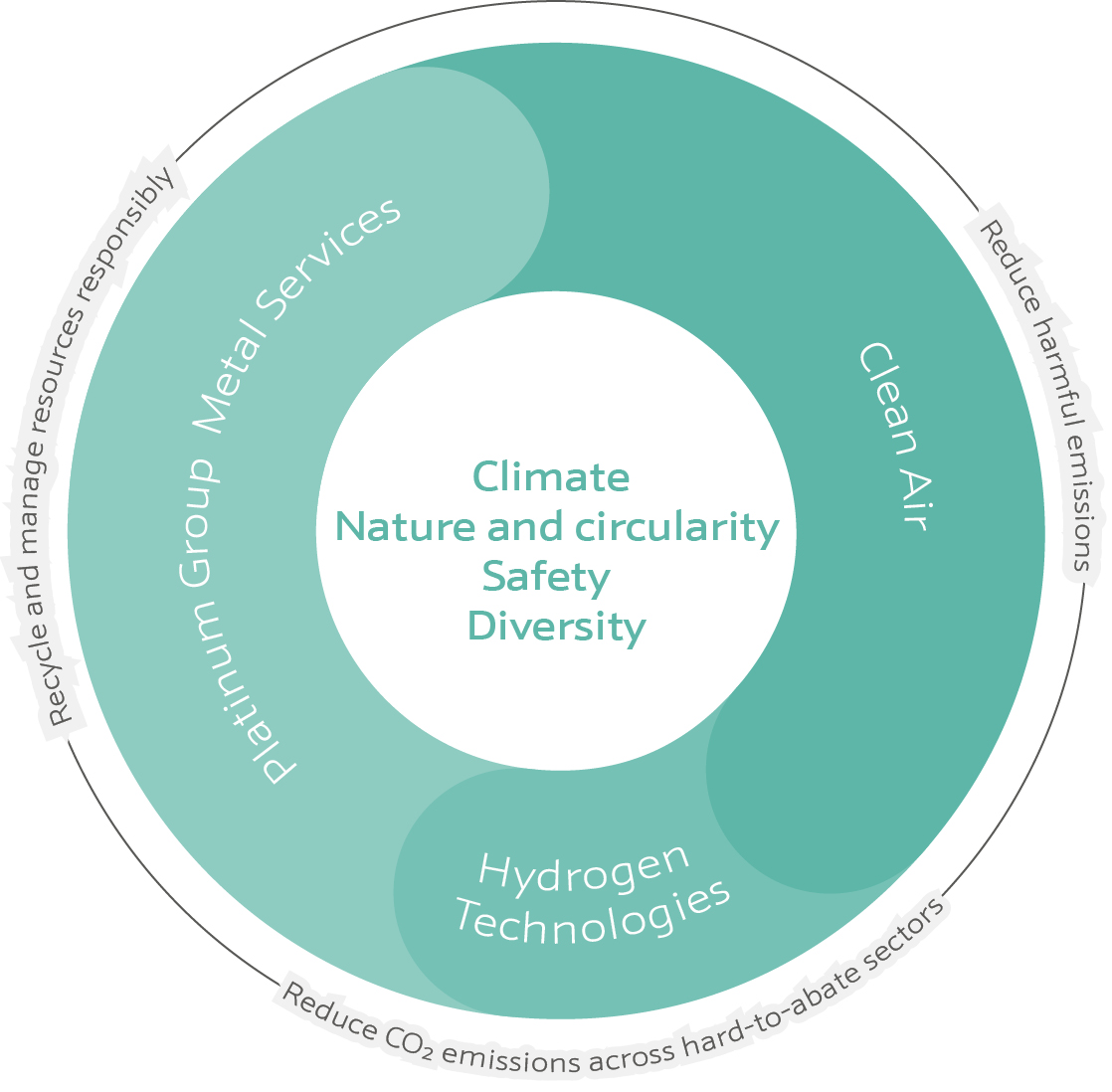

Sustainability is fundamental to JM's strategy. For over 200 years, our expertise in metal chemistry has helped to solve some of the world's most complex challenges.

As expectations around sustainability continue to evolve, we are adapting accordingly – taking a pragmatic, agile and commercially grounded approach to environmental, social and governance (ESG) matters.

Our sustainability priorities — climate, nature and circularity, safety, and diversity — are embedded into how we operate, how we manage risk and how we allocate capital. By integrating these priorities into decision-making across the business, we strengthen resilience, support innovation, and create long-term, sustainable value for our customers, employees, investors and wider society.